2/4/2014

“I was completely

|

|

|

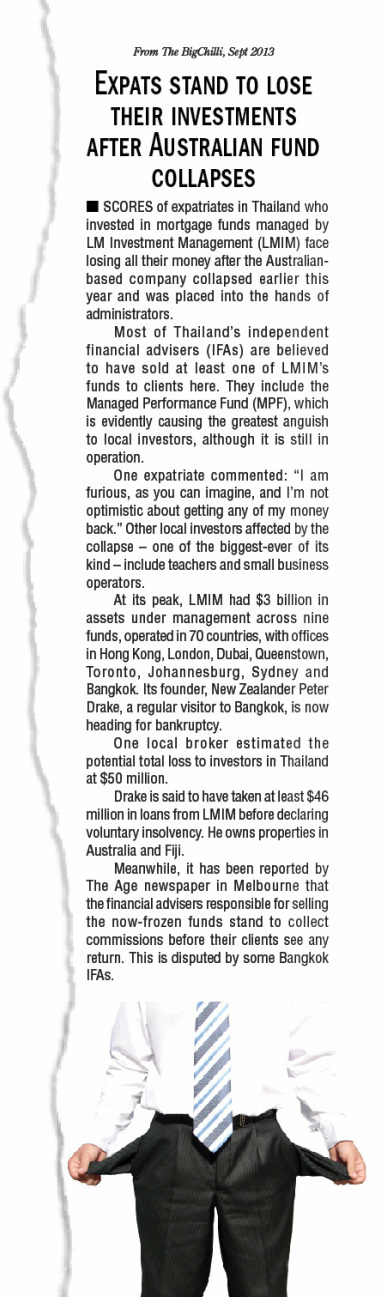

JUST over a year ago, on March 19, 2013, longtime Bangkok expatriate Roy Fox received a telephone call at his home that would change his life forever. It was, he says, the call that one always reads about and dreads, but never expects.The caller was an independent financial adviser (IFA), a fellow Brit and Bangkok resident to whom Roy had entrusted a substantial portion of the savings he had carefully built up during a 40-year career spent working in Europe and Asia.

“I’ve got something to tell you,” said the caller, somewhat nervously. “What’s up, Mike?” asked Roy. “I’m afraid I have some bad news. I have to tell you that LM Investment Management (LMIM) has gone into voluntary liquidation.” Roy froze. He recognized instantly the name LMIM, and he knew exactly what “voluntary liquidation” meant. |

financial advisory companies that had been marketing LMIM in Thailand for several years, it was his job to repeat this same conversation to the many other expatriate clients whom he had also persuaded to put their savings into this now-defunct fund.

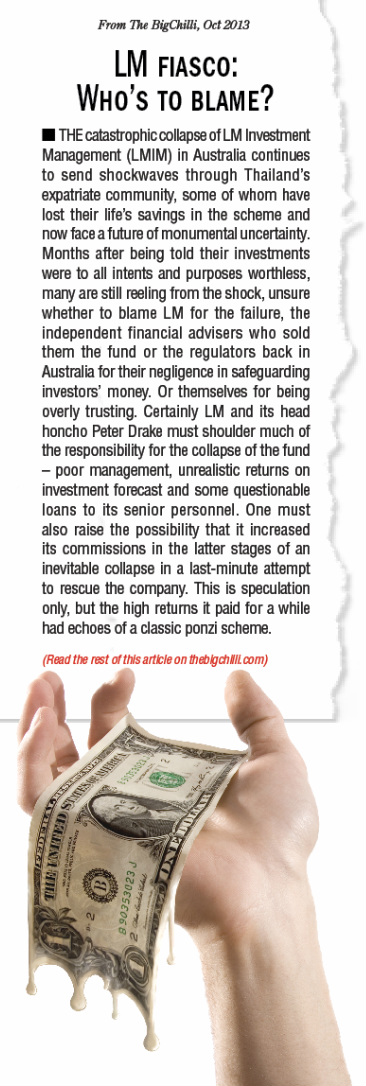

During the following months, LMIM’s spectacular collapse was the subject of intense media scrutiny along with drawn-out investigations by Australia’s corporate watchdogs. Some serious finger-pointing at those believed responsible for the loss of so much money was carried out by administrators both here in Thailand and in Australia as anxious investors searched hopefully for ways to reduce their losses while trying to come to terms with their worst financial nightmare.

One year later, far from resolving anything, the investigations appear to have all but dried up. Peter Drake has faced nothing worse than having his passport seized and certain assets frozen. There’s even an unconfirmed report of him resuming his career in finance.

Most disturbingly, though, it looks increasingly likely that investors in LMIM will not even receive a small percentage of their money from the administrators – especially as their savings apparently rank behind the fees of the IFAs, the very same people who recommended the useless investment in the first place.

So how did an intelligent, worldly businessman like Roy get involved in LMIM? How was he persuaded to part with the best part of his savings to invest in an ultimately dud company?

Trust is the core issue here, says Roy.

“You put infinite trust in people like lawyers and doctors, and it’s the same with so-called financial advisers. They speak in the same professional way and you believe in them because they’re very clever at gaining your trust.

“Was I that stupid? Should I have believed their promises? These are questions I keep asking myself. My family didn’t believe that we had lost so much of our money. They berated me, that the family’s ‘jewels’ had gone literally in a second. It’s taken me nine months to understand what I did. But like so many others, when I first started investing, I thought it was the correct thing to do.”

Roy, who describes his background as “modest, typically British middle class,” says the investment was part of carefully laid plans to provide long term financial security in later life.

Retirement is, of course, no longer an option. Now in his 60s, Roy will have to continue working for the rest of his days, due to LMIM’s collapse.

“People in their 40s and 50s still have maybe 15 years’ working life to recover their losses. But for those of us in our 60s, close to pensionable age, the bell has gone – our working lives should be over. But we can’t stop working. It’s terrible. We’ve been slaughtered.

“The thought of a peaceful, contented time at this stage of my life has been replaced by worry, headaches and fear of financially surviving and getting through day by day.

Roy took the fateful decision to start investing in 2006, two years after ending a lifelong career working for major corporations.“I decided on a completely different career path and financial security was of paramount importance. My new life would mean losing the financial protection a big company had given me – a package that included a regular salary, car and a pension.”

He met Mike through friends who recommended him “as a good bloke who could be trusted.”

“After further meetings, I decided to take his advice and began investing through his company. Basically I wanted a better return on my savings. My one caveat to Mike was that my principle – my savings – should not be touched.

“I told him that I had heard about other people being burned by IFAs, so I was naturally somewhat suspect about the investment. I kept telling Mike to safeguard my money, which, naturally, he agreed to do.

Why did Roy choose to go with the LM property fund?

|

“The first thing was the reputation and image of Australia as a safe and heavily regulated investment haven. Originally, I was supposed to be investing in a secure and protected currency fund but somehow my investment ended up in a property fund. At the time I didn’t question this, but today I am suspicious and wonder whether someone was doubling their commission by making the switch.“Anyway, after several meetings, I went along with Mike’s advice, even though the last thing I wanted was to put my money at any kind of risk.”

To his credit, Mike was never overbearing in their conversations. “But at the same time he was extremely persuasive,” remembers Roy. “Mike was also enthusiastic about LMIM, using words and phrases that suggested it had a great track record, it was Australian and heavily regulated – in other words, rock solid, like a bank. “I checked with others who had invested in LMIM and they too believed we’d be looked after. “We were promised good returns on our investment, and the only proviso was that after one year, the rate of interest could be changed.

“During mid-2011, LMIM offered us a three-year term with annual returns of 9%. Till then I’d been getting 7-8%. At this stage, nothing looked untoward about LMIM, but, shortly after, the rate we’d been promised dropped from 9% to 8.5%, which I didn’t object to, as I realized that we were dealing with market realism and rates could change. “I didn’t know much about LM’s property fund, but always thought it was officially regulated by Australian authorities. But it wasn’t. One of the biggest accusations today is how Mike and other IFAs were able to sell a fund that was not regulated and targeted at people nearing a pensionable age. “I understood that the fund was originally set up to generate funds for property mortgages. I had no reason to question it at first since there were no whispers or gossip about its viability. But I did get a horrible sinking feeling, a premonition of sorts, back in 2012 when I suddenly thought of the consequences to me and my future if the fund were to collapse. But my worries soon passed as I continued receiving my monthly interest payments and everything seemed OK.” Did Roy ever check on Peter Drake and his company? “Yes, I checked their website regularly and I talked to friends and other investors. Nobody expressed any kind of concern. |

|

Yet there were signals that not all was right with LMIM. Explains Roy: “Sometime in July 2012, I received an email from them, mentioning late interest payments and return on capital. The following day Mike called me and tried to cover up the email’s contents. I challenged him, but he merely brushed off my worries, saying LMIM sent it out by mistake.

“Nothing happened and everything seemed normal right up until the day I received that call from Mike telling me the game was over. LMIM had collapsed. I was mortified. My lifetime savings had gone.

“Over the next few months, the situation was given a positive spin by LMIM on its website and by Mike, who was very confident that we’d get back at least 50% of our money. This was cold comfort but it did offer a glimmer of hope that I’d recover some of my investment.

“Later, the administrators put out a bulletin saying that LMIM had very little in assets and what it did have was hyped, overvalued and misrepresented.”

From today’s perspective, what does Roy make of LMIM and its property investments? “In my mind, the fund was nothing more than a ponzi scheme – a complete fiasco.”

Roy is one of many expatriates based in Thailand who committed money to LMIM through a number of local IFAs. In his case, the sum involved was substantially more than half his savings. Others put in huge sums, as much as half a million US dollars or more, while some invested smaller amounts that were nevertheless painful to lose.

For Roy, his experience raises many questions. For example, did any of the IFAs really check what LMIM was doing and how it was performing? “It seems either they couldn’t or didn’t want to,” is his assessment.

“The entire episode is scandalous. I feel very deceived and very angry. The IFAs behind LMIM should together be made accountable.

“Looking back now, it appears from information provided by the LM Investor Victim Centre that LMIM was already in trouble back in 2009, so why didn’t the IFAs take heed of it?

“Also, looking back, I don’t know how I got sucked in. Nor do other investors I’ve spoken to. We’re all at a loss to explain.”

Roy, who says he eventually managed to get a small apology out of Mike, now suggests that the term IFA is misleading. “They don’t advise – they just sell. They have no ethics, and when things go wrong, they’re all over the place.

“But these same IFAs are still running around in fancy cars and enjoying an enviable lifestyle. They’ve not suffered at all. There’s no remorse, no heart. I sincerely believe they should give back the commissions to help compensate investors. But I also know it won’t happen.”

|

What about Mike – is it possible that he knew about LMIM’s impending collapse?

“Peter Drake was apparently in Bangkok on several occasions so some of these IFAs must have had a close relationship with the mother company and surely they would have inquired about the fund’s performance?” Even Roy admits that may not be the case. “The IFAs were still selling LMIM the day before the fund collapsed,” he says. “For me, that’s real incompetence.” The administrators appointed to handle LMIM have added to the furore. In its report, FTI Consulting said: “From our investigations to date, there is evidence to indicate the company may have traded whilst insolvent for a period and entered into certain transactions that may be voidable against a liquidator.” With both his capital and monthly payments gone, Roy was unable to meet various financial obligations. As a result, he was forced to take out expensive loans to pay for bills – a situation he thought he’d never have to face. The effect was devastating. “I lost confidence in myself, got sick and couldn’t work for several months. One’s belief in self-judgment is shattered. All my plans about retirement, taking time off to travel and relax – they’re all gone. “Now I have to watch every penny. I feel very bitter. And I’ll have to work forever. “Luckily, I don’t have children. Other investors in LMIM do – so how are they going to pay when their kids are halfway through schooling or university? They’ve been slaughtered overnight.” Roy is not optimistic about clawing back any of his money. Since the fund was not designed for Australian nationals, he believes the authorities there are not really interested in the situation and would prefer to sweep it under the carpet. Today, he is still trying to come to terms with his losses and what they have done to his life. Many questions still need to be asked, he believes. For instance, was LMIM ever properly audited? Wasn’t its board of directors aware of its precarious position?” |

“It beggars belief,” says Roy.

He’s also critical of the Australian Securities and Investment Commission (ASIC), which issued a statement in April of last year revealing that the LMIM fund was unregistered. “This is a real disgrace,” he adds.

Amazingly, Roy still gets several calls a week from IFAs. Nowadays he knows exactly how to handle them.

For more information about LMIM, go to https://sites.Google/site/investorvictimcentre

*Names in this article have been changed

This is how one financial planner in Thailand marketed the property fund, stressing that Australia has “some of the world’s best performing property markets” and adding that LMIM “has a track record of managing returns in this asset class for more than 14 years.”

• Since the fund’s collapse in March last year, the administrators FTI Consulting have charged $2.4 million in fees, or $130,000 a week. Disbursements came to another $2 million.

• Action against LMIM’s other directors – Francene Mulder, Katherine Phillips and Eghard Van Der Hoven – is being considered.

• EuroWeekly has reported that in Spain “hundreds if not thousands” of expats living on their investments were caught up in the scam, with many now having no money to live on.

• Cyprus-based IFA Scott Kennedy persuaded 180 people to invest in LMIM while pocketing 10 percent commission on the deals, according to the Daily Record newspaper. But Kennedy, 54, insisted that his commission of £1million has been put back into a pot to help investors with legal fees. He says he lost a £355,000 investment in the collapse.